The world’s top 10 solar photovoltaic (PV) module manufacturers shipped a record 500 gigawatts (GW) of modules in 2024, nearly doubling the previous year’s volume, according to Wood Mackenzie’s new Global Solar Module Manufacturer Rankings 2025 report. Despite this surge in shipments, the leading players collectively reported losses of US$4 billion as revenues declined significantly year-over-year.

“In many ways, 2024 was a year of survival through scale for the industry,” said Yana Hryshko, head of global solar supply chain at Wood Mackenzie. “Aggressive pricing, intense competition, and continued capital investment weighed heavily on margins as companies pursued long-term leadership in market share and technology.”

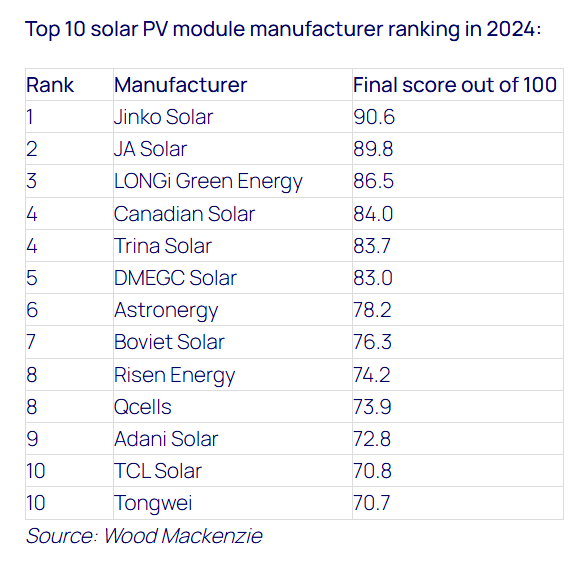

Top players maintain strong output amid market pressure

Wood Mackenzie’s score-based ranking assessed more than 40 leading module manufacturers across 10 countries. These companies accounted for 62% of global production capacity and 89% of global module shipments in 2024, highlighting the concentrated nature of the industry’s top performers.

Despite challenging market dynamics, the top 10 manufacturers maintained a strong average utilisation rate of 69%, reflecting efficient operations and steady demand for their products. This performance underscores the resilience and competitiveness of leading manufacturers in competitive pricing environments.

Geographic expansion key to navigating trade challenges

According to Wood Mackenzie’s report, China continues to dominate the solar module manufacturing landscape in terms of scale, but emerging challengers from India, South Korea, and Vietnam are rapidly closing the gap as global production becomes more geographically diverse.

This year’s rankings introduce a new criterion to evaluate manufacturers’ ability to navigate rising trade tensions and country-specific market barriers. Seven of the top 10 manufacturers now operate production facilities in three or more countries, including Cambodia, India, Malaysia, Mexico, and Vietnam. Looking ahead, several top 20 companies are expected to expand into Egypt, Oman, Saudi Arabia, South Africa, Qatar, and the UAE.

“Establishing production across multiple countries allows manufacturers to navigate tariffs, local content mandates, and import barriers,” Hryshko added. “It’s a strategic move to remain competitive in an increasingly fragmented global landscape.”

Vertical Integration Advances As Manufacturers Target Upstream Control

Wood Mackenzie’s latest rankings also highlight a growing trend toward full vertical integration among leading solar supply chains. While cell integration is now standard among top-tier module producers, several companies are accelerating investments in wafer manufacturing to gain end-to-end control over production.

“The most ambitious players are moving upstream into wafer production,” added Hryshko. “This strategy enables tighter control over cost, quality, and compliance, especially in a complex trade environment. As a result, reliance on third-party wafer and cell suppliers is expected to decline, reshaping the upstream supply landscape in the coming years.”